I’m believing that more than half of money spent by government is fraud, and half of what is left is unnecessary crap. A million bucks for 30 square feet of sidewalk? For climate change?

A comment to my post on cashing in:

Very enlightening. Up to now, I assumed it was big pharma and greedy insurance companies that caused health care costs to skyrocket. The correct answer, as it turns out, is all of the above; everything connected to healthcare.

No offence to oldvet, this post isn’t an attack upon him, but is a classic case of supply and demand. The ED wants to open, but there is a shortage of qualified nurses. They have no choice if they want to stay in business- by law, an emergency room has to be open 24/7. So they have to:

Since the US has a climate of legal liability, medical care is a field that has zero room for errors. People who can treat patients without making a single error are rare and in high demand. That means there is a bidding war for their time.

Skilled people cost money, which is why it costs $165 to have a plumber snake a drain. No one wants to look up while having a medical emergency and see the cheapest nurse caring for them- they want the best, or at least someone who is good at what they do.

It takes 3-4 years to train a basic nurse. More than 3/4 of those who begin the education don’t make it.

Then it takes another year to train for the ED specialty. Two more years before they reach a point of proficiency without needing guidance and supervision.

Of the nurses here who manage that seven year slog, just over ten percent are good enough to be board certified in emergency medicine. Only a quarter of those have two board certifications.

In other words, of the 257,000 actively licensed RNs in Florida, 17,000 are Emergency Room nurses. Of ED nurses, only about 2500 of them are board certified. Only about 800 of them have two certifications.

Are two specialties really needed? Certified Emergency Nurse, sure. How about a nurse certified in stroke care? Pediatrics? Trauma? Vascular access? Critical care? Each of those is a subspecialty that is needed in the ED on a daily basis.

Now consider that there are 477 licensed emergency departments in Florida, all competing for those nurses. Everyone wants the best, so those who have multiple certificates and degrees demand (and get) top dollar. My last employer had 162 ED nurses and still didnt have enough for their patient load. That drives up costs.

They only way to eliminate the nursing shortage is to either lower demand or increase supply. Lowering demand isn’t going to happen. Raising supply can be done in two ways:

In today’s legal climate, lowering standards would actually cost more in increased litigation caused by more medical errors. In the ED, 95% of patient care is performed by nurses. We write orders for imaging, lab work, and treatment. What kind of provider do YOU want at your side during your next medical emergency?

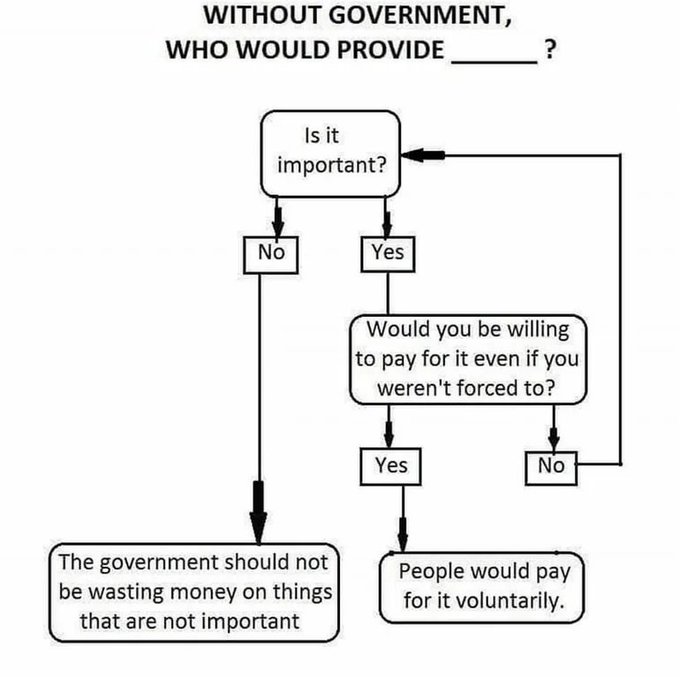

A recent post looked at the out of control spending of Cape Canaveral. Both parties are busy screaming about how the proposed elimination of homestead property taxes are going to cause police, fire, and schools to be shut down.

That’s a lie.

The problem isn’t police, fire, and schools, although I think we spend too much on those services. Cities and counties are busy spending money like a 16 year old who just found his dad’s credit cards. I want to give another example: Orlando.

In 2015, the city of Orlando has a population of 270,000 and a budget of $1.1 billion. That’s bad enough at $4,200 per resident, but let’s fast forward to 2025. In the year 2025, Orlando’s population had increased by 22% to 330,000, but the budget had increased by 63% to $1.8 billion, or $5,300 per resident.

The median household income in Orlando is $72,336. Median individual income is $43,312. The median property tax bill in Orlando is $3,413, or about 5% of annual household income. Too high.

This is the out of control spending that needs to be brought under control. For years, we have asked cities to control spending, but they have told us there is no room for cuts. Well, I am going to do my best to get this passed and force cities to make the cuts they should have made years ago.

The time of people who vote for a living stealing money from people who work for a living is going to come to an end in Florida if I have anything to say about it.

Let’s contrast this. Here is a leftist:

Now let’s compare that post to this one from a prominent Republican who is opposed to the elimination of Florida’s property taxes. Click on this link to read the entire conversation: (this was removed due to confusion between two similar sounding names.)

There is no functional difference between the Democrats and the Republicans. Both parties want to take your money. The only difference between the two is which set of cronies are the recipients of your tax dollars that they they return to the party in question. It’s all a big lie.

I’ve said this tons of times: just because Democrats are your enemy doesn’t mean that Republicans are your friend. I’m sick of both parties, as all they do is take my money and my freedom while telling me it’s for my own good, because they know how to spend my money better than I, but it always seems to benefit them more than it does me.

Party of small government and fiscal conservatism, my white ass. I may just return to my previous philosophy of “voting for the lesser of two evils is still voting for evil” and not vote for candidates of either party. I will, however, vote to cut taxes and strip the government of powers at every opportunity.

I won’t vote for a Democrat, but Republicans are going to have to earn my vote. Give me a reason to vote for you- don’t just talk about being small government, prove it.

The two most prolific opponents of cutting Florida property taxes I see on my feed are Jeff Brandes and Holly Bullard.

Holly Bullard is the chief strategy and development officer of the same institute. Her job is directing fundraising, policy advocacy, coalition building, outreach and communications strategies. She makes $110,000 per year.

Florida Policy Institute is a left of center NGO that specializes in collecting government grants, as far as I can tell. Their funding is part of a nearly impenetrable web of grants and untraceable funding. It appears to me as if it were another grift.

Ever since DeSantis came out with his proposal to virtually eliminate property taxes, by social media feeds have been absolutely overrun with people screaming about how towns will go bankrupt and have to shut down police, fire, and roads. It is so pervasive and widespread, it’s like a chorus. They are also being misleading.

I want to use my town as an example. For a reminder on how Florida does property taxes, you can read this old post from a year ago. Where I live is a town with 3500 people living in about 900 households. Our only commercial property consists of a convenience store and a single diner. Of those households, nearly a quarter of them (18%) pay less than $200 a year in non-school taxes.

Town revenue breaks down like this:

Keep in mind that the town LOVES my neighborhood, because the people in it comprise only 1/10 of the town’s population, but pay about 25% of all ad valorem taxes. Another 18% pay nothing, or nearly so. The governor’s plan would increase homestead exemptions to $250,000 (from $50,000 currently) in the first year, then to $500,000 the second year, meaning no one would pay taxes on any home until its value was more than $500,000, except for school taxes, which would remain unaffected. A complete loss of ad valorem taxes on homestead property would mean the city would face a loss of 14% of their revenues. What would have to be cut? Let’s look at the town budget. This is where the town budget goes:

It seems to me that the town is pretty top heavy in administration, the library is an extravagance, and I would argue that a town of 3500 people doesn’t need 15 police officers. I would cut the library, and I would cut the police and admin budgets by 10% each. That takes care of most of the cuts you need right there.

The town has 50 employees, with 15 being law enforcement officers. Granted, 20 of the town’s employees are seasonal or part time, but that seems like a heavy dead load for a town of 3500, where a fifth of them aren’t paying any taxes at all.

Since 2020, the town’s total revenue has increased 250%, but the population has only increased by 6%.

Losing ad valorem taxes on homestead property isn’t just doable, it’s the only way to curb the bloat. Towns are treating these massive windfalls from taxation like a teenager who just found his dad’s credit cards.

Kevin O’Leary tells people not to waste $28 a day on lunch.

He is immediately scorned because, the people who are struggling complain, then produce excuses as to why they need those $28 lunches. Do the math:

If you go out to lunch at $28 a day every workday, that works out to $560 per month in lunches. What if you had brown bagged it every day instead? That could easily free up $350 per month that could be invested. In an index fund at 9% per year, that adds up.

Or you can keep going out and spending $28 a day on lunch, $5 on a Starbucks every morning, and complaining about how you are still broke and blaming “boomers” for the fact that you can’t afford to buy a house.

The Chicago Cubs are suing a bar located near their stadium, because the bar isn’t paying the Cubs for allowing their customers to look at the team while they play baseball. The team is claiming the rooftop bar is misappropriating the team’s property rights because the bar is selling admission to the bar and allowing patrons to watch Cubs games from that vantagepoint. It looks like the courts are going to side with the team. In the meantime, the city is investigating the structural integrity of the roofs, issuing citations to those in danger of collapse. I’m sure those investigations are totally legit and were in no way sponsored or encouraged by the billionaire team owner.

Money talks, I guess.

The Ricketts family, billionaire owners of the Cubs, began purchasing the nearby rooftop properties in order to control the marketable sight lines into the stadium and by the end of the 2016 season, owned (or controlled via agreement) 11 of the 13 rooftop locations that had a view into the nearby baseball field. Wrigley Rooftop is one of the two that has thus far refused to sell.

I don’t care what the court says, if I can see it from my property, then you have no claim to force people to pay for looking at it. This will open all sorts of legal maneuvering. If my neighbor can see into my yard, can I sue him for watching me swim in my pool?

If the Cubs don’t want people in nearby tall buildings watching them play, perhaps they should build a dome. I’m sure they can get taxpayers to foot the bill. After all, teams build sports ball complexes at taxpayer expense all the time. For example, the Tampa Bay Rays are getting a Billion dollars of taxpayer money to build their new stadium, even while the local governments of the state are assuring the taxpayers that property taxes are totally needed to fund things everyone agrees are needed- things like firefighters, police, schools, and roads: “The money we take in from property taxes totally is being used for needed services and is in no way being used to fund billion dollar sports complexes. The money going to build places of business for billionaires to pay millionaires to play children’s games is totally coming from a different line item that was totally taken from taxpayers in a different way, so it doesn’t count.”

If that doesn’t work, perhaps the team could try the Scooby Do method and pay someone to dress a ghost in order to force the owners to sell.

Meanwhile, the shortstop for the Rays is being paid $182 million to play baseball. Jason Heyward is being paid $184 million to play the game by the Cubs. Meanwhile, the bar in question (Wrigley Field Rooftop Bar) is estimated to be making $1 million a year.

This is one of those times where a billionaire is doing something immoral to make more money, and the government shouldn’t be getting involved. Government should not be in the business of picking winners and losers. Remember, when the legislature decides what can be bought or sold, the first thing to be bought and sold are the legislators themselves.

In case you were wondering why today’s youth complain about the high cost of living…

Spending money on their idea of LOOKING rich for one night.

We keep being told how eliminating property taxes will mean roads, the fire department, and schools will be unfunded. They tell you so because everyone wants those services, but here is a great example of where property taxes go.

That’s right- Hillsboro county is going to use a billion dollars of taxpayer funds to build a new stadium for the Tamp Bay Rays. That works out to nearly $2,000 per household. They powers that be claim no one will notice, because the billion will come from county reserves. See, you won’t notice how we stole a bunch of money from you so we could pay a bunch of grown men a hundred million apiece to play a child’s game.

Incidentally, the team is worth $1.7 billion, but the taxpayers are expected to build half of the $2.8 billion stadium they will play in. How about instead, we let the taxpayers keep their money, and the team can charge what the traffic will bear for tickets instead of forcing taxpayers to fund your business?

EDITED TO ADD:

If the new field lasts as long as the old one, the stadium will cost $80 million for each year it’s used, or about $1 million per game. There are 25,000 seats in the stadium, meaning the team would have to add $40 to the price of each and every ticket to pay for the stadium themselves. That seems reasonable to me, and if people won’t pay it, then does Tampa really need baseball?

The standard argument about getting rid of property taxes is always “Who will pay for Fire Dept, Police, Schools, Roads?”

Even so, the proposed law would cut non-school ad valorem taxes for homestead property. Schools won’t be touched, as they are exempt. How about the other services?

Let’s use Daytona Beach as an example. You will see why I chose Daytona shortly. Daytona Beach has adopted a $379.8 million budget for the 2025-26 fiscal year (beginning Oct. 1, 2025), a 4.1% increase in property tax revenue driven by rising property values. The budget holds the millage rate at 5.9300 ($5.93 per $1,000 of taxable value). About a third of the city budget is from ad valorem (property) taxes. However, only a third of ad valorem taxes are from homestead property. The vast majority of property taxes are paid on commercial property like hotels, stores, and rental property. Overall, the loss of homestead ad valorem taxes would only cut city revenues by about 12%.

In Daytona, police and fire take up 55%, roads are about 15%, and schools take up 0% of the city budget. That means expenses that aren’t fire dept, police, schools, or roads comprise 30% of the city budget. In other words, the 70% of the budget for the police, fire, schools, and roads wouldn’t be touched if property taxes on owner occupied homes.

Especially if you consider that those departments are filled with waste, fraud, and corruption. One firefighter in Daytona blew the whistle on the department cooking the books and wasting damned near a million bucks a year. What did he get for his efforts? He was terminated. What’s going to happen there is he will sue the county and will likely get a huge paycheck because it is illegal to take action against a whistleblower. Somehow, my tax dollars will pay for the corruption, and will also pay for the lawsuits resulting from that corruption.