The FED, as the US central bank, can’t restrict the money in circulation by increasing interest rates as long as the Federal government increases spending by 16% year over year.

economics

Thanksgiving Costs

Here is the claim being made by the left:

Now for the facts. Here is what it costs to feed ten people for Thanksgiving for the past 33 years:

The cost may be down from last year, but Thanksgiving is still 30% more expensive than it was for Trump’s last Thanksgiving in office.

economics

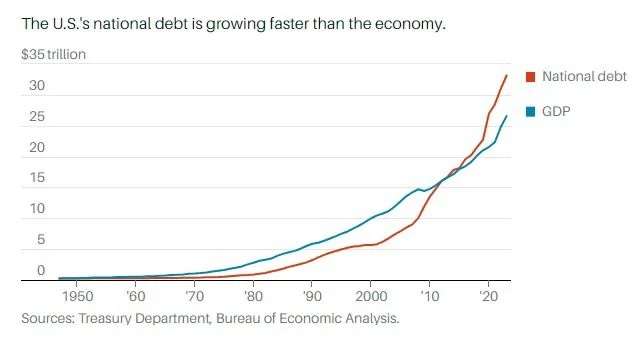

Leaving the Dollar

The yields on Treasury bills hit a 16 year high, and they aren’t done. Inflation in the US is killing confidence in the dollar. China has been engaged in moving away from holding US treasuries. They have sold off many debt holdings, going from holding $1.3 trillion in US debt to just over $800 billion- a downsizing of about 40%.

All of this is making it more and more expensive for the US to pay the interest on the $33 trillion that it already owes, and will soon begin affecting the strength of the dollar. The US will have to create money out of thin air in order to cover this as well as still keep sending money overseas. Expect more inflation to come as a result.

economics

Trois Bés (Three B’s)

When you read that the US is now paying more in interest than it spends on national defense, you can rest easy knowing the facts:

“The Federal Reserve owns a lot of government debt,” Braun said. “The Treasury does pay interest payments to the Federal Reserve, but then the Federal Reserve turns around and gives it back to the Treasury — that alleviates some of the issues.”

So we are just paying ourselves? Oh, nothing to worry about, then. We can just borrow another $30 trillion. It will be fine. Take a look at what the milestones the debt has hit over the past year or so:

| Date: | Amount of National Debt | |

| October 12 | $33.5 Trillion | |

| September 15 | $33 Trillion | |

| July 11 | $32.5 Trillion | |

| June 15 | $32 Trillion | |

| June 2 | $31.5 Trillion | |

| Sept 30, 2022 | $31 Trillion |

This time in 2019, I was posting that the national debt was at $23 trillion. We have borrowed more than $10 trillion in the past 4 years, with a $2 trillion of that being in the last 4 months. The rate of growth in our national debt is exploding.

The debt is growing far faster than the economy. So much for Keynesian economics. We are fast approaching the point where our national debt is 1.5 times the size of GDP. There is no recovering from this. There is no way to pay this off. The only outcome now is economic collapse. The only question is when.

I don’t understand what is going on and why the Feds are on such a spending spree, but what I do know is that this isn’t good. If you look, the US was borrowing about $2 Trillion a year until June of this year. That was scary enough, but there are some serious problems coming up, as this country (with the exception of the pause in the debt ceiling in August) is now borrowing a trillion bucks about every 60 days. This can’t continue, and by definition, anything that can’t continue, won’t.

There is going to be some major inflation coming. Our currency is being devalued like never before. Stock up on the three B’s: Bullets, Beans, Bullion. They are about to become a whole lot more valuable.

economics

The Economy

A couple of you asked that I talk about the squeezing of the middle class. When the left first began screaming about increasing the minimum wage back in 2013, I explained that employers would respond by compressing pay, because economics forces them to.

Employers can respond to wages that are rising through one of two means. The most obvious way is by increasing prices. The problem with increasing prices is that there is a limit to how much that can happen. Let’s say that the minimum wage is increased to $26 as the left is now requesting, or even the $33 an hour that New York City is looking for. McDonald’s will just increase the price of hamburgers, right? That works, but only to a point before people shop elsewhere for their burgers. Still, the left will argue that, since EVERYONE will get this new wage, all of the restaurants will increase, and people will have no choice. The people who say this forget that McDonald’s isn’t just competing with Burger King and Wendy’s; they are also competing with people simply brown-bagging their lunch to save money. There is a price point where people simply stop eating out. This greatly reduces economic activity and creates things like stagflation. Soon, it is only the upper half of the income scale that can afford to eat out.

The second way that businesses fight rising minimum wages is through pay compression. The business only raises wages for those whom they are legally required to increase. This causes the skilled laborer to make the same money as an unskilled one, thus removing the incentive for skilled labor. This incentive for people to remain unskilled soon squeezes some from the median of the middle class towards the bottom.

So how do we fight this? We can’t keep thinking that we can vote or legislate ourselves out of this. Instead, we need to be ready for the future. How do you prepare for the things that are coming? We aren’t going to see some Mad Max type of nationwide collapse. That just doesn’t happen when a country’s government collapses. What happens is that governments get replaced with something else, and building wealth is usually going to do more for you than wasting your time complaining about how rich white guy boomers are stealing the jobs from you that you weren’t qualified to have in the first place.

You need to recognize the trend. Look at the facts: right around 4 million teens graduate from high school each year, with half of them directly entering the work force. If all you have is a high school diploma, what are you doing to make yourself more employable than they are? What makes you special?

To make that even worse, there are currently about 10,000 illegal immigrants entering the country every day. A good portion of them have skills like construction and landscaping, and let’s be honest, are willing to work for less than minimum wage.

Your labor is a product being sold on the free market, so what makes your application look better than the next guy’s? It’s even harder if you are not one of the special class of people that the FedGov is telling employers that they must favor. That doesn’t mean you need to go to college, it means that you need to have job skills that will make you more employable, and you need to make sure that those jobs skills are in a field that will land you at the median income to start, and will allow you to make more money as time goes on.

In some cases, that means college. Not any college degree will do- you need a degree in something that is actually useful. STEM fields are good choices, so is a degree in human resources, but the field there is crowded, so be careful. Firefighting was a good career for me, but that depends on where you live. You could learn a trade. The Mike Rowe Works Foundation is a great place to start.

Mike Rowe says, and I agree with him, that we in this country have a problem: We have made work the enemy. It takes hard work and self control to become financially successful.

When I was a teacher, I would try to give my students this talk. I would ask them what they wanted to do, and I would get replies like

- video game designer

- Social Media Influencer or Youtuber

- Professional Athlete

- Doctor

I would then ask them how they were going to achieve that:

- Have you designed any simple ones yet? Like perhaps an app?

- How many videos have you made already? How many have gone viral? Do you already have more than 100,000 followers?

- How many hours do you practice your sport each day?

- How are you going to become a doctor if you can’t even manage a grade higher than a C in high school biology?

The answers were predictably disappointing. There was nothing for the game designer except the love of playing video games. The Youtube and social media fans hadn’t made any videos yet, or if they had, those videos had less than 1,000 views. The athletes didn’t practice outside of what the high school required for their sport. Everyone wants to be rich and successful, but far too many people aren’t willing to go the extra 5 miles that it takes to truly get there.

The point here is that you should treat yourself and the labor you produce as a product. Make your labor something that you can sell for a good price. Don’t sit on your ass waiting for someone to knock on your door and offer you big money to play video games and write crappy leftist poetry. There aren’t enough of those jobs for everyone. If you want to make more than average, you and the product you are producing have to be more valuable than average.

I can’t tell you what job you should be doing, or how you should do it. I am just telling you what you have to do- you have to put in the effort, work hard, and be patient. It takes decades to become financially wealthy.

- Your 20s are going to be a struggle. You are learning skills, or should be. Don’t be paying for $2,000 in tattoo work when you could be investing that money in your future. Education, financial investments, and other things that pay off later. Not useless baubles that will not do a thing for you. Most people don’t have an earning problem, they have a spending problem. Control spending and invest.

- Your 30s will be a bit better, but you have to resist the temptation to spend your money and take out loans against your future earnings to buy things that will be gone in a year or two, or in buying useless items like a Rolex or flashy clothes.

- Your 40s is where you really begin to build wealth. You can relax a bit on buying things for yourself, but you still need to keep the useless spending under control.

- The 50’s is where you hit the peak of building wealth. By age 50, less than half of Americans have a net worth of more than $315,000. Try to be one of them.

- The median wealth of a 60 year old in the US is $500,000. The mean net worth of a 60 year old is $1.6 million. You can get there, but it requires that you be smarter, work harder, and avoid useless spending when you are young.

Above all, don’t waste your time bitching about what others have. The fact that others are richer than you isn’t hurting you at all. One man being rich isn’t preventing you from being rich as well. Instead, you should be asking yourself why you aren’t doing better. Are you wasting your time instead of working to make more money? If you have 10 hours a week to play video games or surf the web, perhaps you could put away the child’s toys and take some classes.

Or is it that you are wasting your money on $5 Starbucks coffee, a $400 tattoo, or designer clothing? How is buying things that make you poorer going to help you become financially richer?

Be honest with yourself. Don’t fall into the trap of making excuses for your lack of work and thrift. The only person who will be harmed by those behaviors is you.

Price Controls

Minimum Wage

Today, the minimum wage in Florida increased by $1 per hour. The minimum wage for non-tipped employees in Florida is increasing from $11 to $12. For tipped workers, the rate’s going from $7.98 to $8.98.

Minimum wage has increased from $8.56 per hour to $12 per hour in three years- that is a 13 percent annual increase. I still can’t go through a drive through without them screwing up my order, and in that same time period, the cost of a Big Mac meal has gone from $7 to over $12- which is a 23% annual increase.

At Denny’s, 2 strips of bacon, two link sausages, two eggs, and two pancakes. This is the breakfast that Denny’s calls the “Original Grand Slam.” Sold for $1.99 in 1997. By 2021, that same breakfast cost $9.49. That works out to an annual inflation rate of 6.7%. Now here we are in 2023, and that same breakfast is now $11.99, or a 26.3% increase in the past two and a half years. That’s a 10.5% annual increase.

Price and wage controls don’t work.

Disney Pedos

The Fall of Disney

Disney has announced that it will be closing its Star Wars themed hotel. The concept of the hotel was complex, and shows a complete lack of awareness of your customer base. The idea was that the hotel would be like living on a space faring cruise ship. The experience was to be totally immersive.

There were problems with the concept that doomed it to failure from the beginning, and these problems would have been easy to spot, if only someone had discussed it with actual people. The biggest problem is the cost: $1,200 per night for the first two adult guests. For additional guests staying in the same cabin, it would be $500 per night for a child, and $700 per night for an adult. To compare, taking a comparable cruise on a conventional cruise ship with complementary alcohol, internet service, and a personal butler costs about half that. The extra cost is for the Star Wars experience.

So what is this experience? It is focused on the time period of the latest Disney versions of the Star Wars franchise. You know, the movies that only the biggest Star Wars geeks follow with enough excitement to go to this hotel. The characters from the original George Lucas time period don’t exist in this time period, so many original Star Wars fans, most notably the older ones with the money to stay here, won’t recognize many of the characters. The very nature of the hotel limited your customer base, which was already limited by the high cost.

As a hotel instead of an experience, it was a total bomb. There was no swimming pool, no gym, nothing but an extended, expensive cosplay of a movie franchise. For this business to be successful, there has to exist a large enough subset of people who are big enough fans of the movies that are able and willing to spend more than $1,000 a night to cosplay a movie while staying in a crappy hotel.

There just aren’t enough people who are large enough fans to do that at a $1k per night price point. Had Disney executives done a simple market survey, this would have been apparent. The failure of this hotel is a microcosm of the failure of Disney as a company.

There is a lot of talk about Disney and Ron DeSantis’ feud, and many are saying that Disney announcing layoffs and cancelling their projects in the Orlando area are signs that Florida’s governor is losing the battle. That’s BS. The real issue, and reason for these cutbacks, is that the current executives are woke morons with no real business sense. They are taking a company that made its mark, and became an industry giant, by selling family friendly entertainment.

Disney once made wholesome entertainment, beginning in the 1940’s with the classic animated stories like those of Snow White, Pinocchio, Dumbo, and Bambi. Then the 1950’s and 60’s saw the company continue with animated movies, but also told live action stories like Treasure Island, The Absent Minded Professor, Swiss Family Robinson, 20,000 Leagues Under The Sea, and Old Yeller. Over the years, we saw other wholesome movies like the Apple Dumpling Gang, the series of films like Herbie the Love Bug, and Escape to Witch Mountain. The films of Disney were so family oriented, that the company’s first film to not be rated G was the 1979 film The Black Hole.

We moved to Florida in 1972, when my father, who worked as an early computer engineer for Hewlett Packard, was sent there to support the new tech boom in Central Florida. I visited the Disney complex for most of my life. I grew up around Disney and its theme parks. On two different occasions, I worked for the company. Once when in high school flipping burgers and loading people on the attractions of Horizons and World of Motion, and again years later as a repair technician, repairing dancing chickens at Splash Mountain.

I raised my own kids on Disney movies: The Lion King, Aladdin, the Little Mermaid, Toy Story, and Monsters, Inc.– Disney was still making quality entertainment that families could enjoy well into the new century. Even as an adult, I used to pay to enter the parks to see attractions like the Osborne Family Christmas lights. I would go to see the Christmas decorations and sip some hot cocoa while listening to Christmas music. It was relaxing to escape and see some wholesome entertainment.

Disney has changed so much from those early, family friendly years. The cracks began with the rise of what is called “Gay Days.” In 1991, a large group of about 3,000 homosexuals flooded the park while wearing red shirts. It wasn’t a company sponsored thing. That would change over the years, and by the end of the ‘oughts, the event would grow to be a company sponsored event with 150,000 flooding a family friendly park with sexual messages- all aimed at kids.

Now the company has broken with its former self, and spends time producing many films that are no longer aimed at families. Now they are aimed at sending a political and sexual message to kids. From changing old characters to new, sexualized ones, the new “woke” Disney is more aimed at destroying the family than it is at celebrating it. There was a time that Disney jealously guarded its reputation. That time is gone.

That’s why the Disney hotel failed, and that’s why the Disney company is underperforming. The company has lost its way. If the company is to be saved, the brand has to return to its family friendly, wholesome roots.

economics

Anthony Oliver & Economic Literacy

Is economically illiterate. He cancelled his show because he won’t do it unless he is paid $120,000, with the venue only charging $25 a ticket.

Don’t buy Cotton Eyed Joe tickets for $99 apiece. Sure as hell don’t buy tickets for VIP passes for whatever bulls–t prices they’re on. Don’t pay $100 for a ticket. If we’ve got to cancel the venue and play somewhere else, we will

Unfortunately this kind of economic self sabotage is common:

- Complains about poverty

- Doesn’t understand money

- Demands $120,000 for a 60 min performance

- Cancels the performance he agreed to do because he thinks ticket price is too high

The venue only holds 1,500 people. Oliver’s take costs the venue $80 for each ticket, assuming that the show is sold out. He moved the concert to a larger venue (Knoxville Convention Center) which holds 10,000 people. Now his take costs $12 per ticket. The rest of the costs of the venue, as well as profit for the venue, have to come from the other $13.

Do you think he learned about economy of scale? Or does he still not understand how money works?

Economic illiteracy is why so many people don’t understand why it is that a business needs to increase prices. That’s why you see people complaining when fast food prices rise. This guy is upset that it cost him to buy 18 items for 4 people at Taco Bell, and it cost him $53.

It isn’t greed, it’s increased costs. We told you that raising the minimum wage would come back to bite you in the ass. Now it has. That’s just economics. The increased costs of wage hikes, combined with inflation caused by poor monetary policy has made everything cost more.

I am in the middle of setting my rent for the coming listing. Since 2020 when I first rented to this tenant, my costs have increased by 22%. (11 percent per year) Over that same period, I have increased rent by 20%. (ten percent per year) For the coming year that begins October 1:

- my landscaping cost will be increasing by 13%

- Property taxes are increasing by 10%

- I’m waiting to see what will happen with my insurance. That bill comes any day now.

Now that the tenants are moving out, I am free to set my rent to market rate. I think that will be somewhere around a 12-15% increase. Maybe more.

Things like this happen, and people don’t understand why prices had to increase. I run a business. Any well run business will tell you that prices are determined by costs. If my costs exceed what I can charge in prices, then the business will go under. People are the same- you are selling a product. Your labor. What you can charge for that labor is dependent upon its value. If you don’t like the wages that you are making, you need to find a way to make your labor more valuable. If not, the customer who has been purchasing your labor will find a way to buy from someone else, or won’t buy it at all.

This also explains why so many people are poor. They don’t understand economics, money, or how to run a business. Many people can’t even balance a checkbook. How can you run the business of your life when you don’t understand money?

economics

Tenants and Bankruptcy

Although he was posting under a fake name because he was trying to evade a ban and is thus a complete asshole, Hedge (posting as “TheMan”) raised an interesting point, one that I am sure he didn’t seriously intend.

When you file bankruptcy in Florida, the automatic stay will protect you from eviction unless:

- The landlord received a judgment of possession prior to the filing of the bankruptcy. A judgment of possession is the final court court order in an eviction proceeding. When this order is signed by the judge, the tenant is officially evicted and the landlord may take possession by legal means. The judgment of possession extinguishes any legal right the tenant had in the lease, thus there are no further actions to stay. If the order was not signed before the bankruptcy is filed, the automatic stay will stop the case from proceeding.

- The landlord files a motion with the court stating the tenant has damaged the property or the tenant has used illegal drugs on the property within the past 30 days, the tenant will have to respond or the stay will be lifted, and the debtor will be fully subject to ALL of their creditors’ actions to collect debt. If the tenant responds, the court will decide after a hearing. Since Bankruptcy Court is a FEDERAL court, and marijuana remains illegal (for now) at a Federal level, weed is enough to meet this standard. If your tenant has a weed card, you can get their stay lifted.

- If the tenant does not make lease payments due AFTER filing bankruptcy, the landlord will be able to get the stay lifted.

- If the tenant does not cure the default on the lease (pay past due rent due before the filing) within a reasonable time, the landlord will be able to get the stay lifted.

A tenant filing Bankruptcy is actually good news, because you know that you are going to get paid from that point forward, with the power of a Federal Bankruptcy court behind you.

economics

Creative Accounting

A blog post from WIrecutter over at Knuckledraggin My Life Away brings us a story about how California landlords are charging fees for parking spots, trash pickup, pest control, use of a mailbox and routine maintenance requests everything they can think of. This is the only sensible response that landlords (or any business) has when a government has inflationary policies coupled with price controls.

The entire situation was created with the double whammy of the eviction moratorium and tax increases. In my area, you can add large increases to property insurance. Any business that has increased costs must recoup those costs by increasing prices. The government responded to that by enacting price controls (rent control). In places all over the nation, landlords are being told what they can charge for rent, even as the costs like property taxes, interest rates, and insurance continue to climb.

So landlords are responding in exactly the way that I predicted they would- they are looking for new revenue streams by charging for perks that used to be gratis. Here is what I said on the matter nearly two years ago when communities in Florida were talking about rent control:

If rent control is enacted, there are steps I can take: Each year, I will raise rents by the highest permitted under the new law. On top of that:

– I will no longer provide lawn service as a part of rent. That will shift $900 a year of expense to the tenant.

– I will no longer provide a free washer and dryer. I will recommend a company that will rent the tenant one at an additional cost, if they don’t have one. That company will be owned by me. The going rate for that is $144 a month.

– I currently pressure wash the outside of the property twice a year. I can push that off to the tenant, and make it their responsibility as a part of cleaning.

There are many ways that I can maintain profitability. Just taking the three steps above will have the effect of increasing the cost of renting by 15 percent without increasing the rent itself.Landlords will have to be creative.

The list is endless. I can have parking stickers made, and I can charge you $15 per month for each sticker. Any car parked on the property had better have a sticker, or there will be a $50 fee charged per day for not having a sticker. If the fee isn’t paid, cars without stickers will be towed. I’m not a jerk, though. Parking in the garage will still be included in the rent.

I offer my tenants a lot of free perks- washer and dryer, lawn and pest control, all included in rent. Many landlords offer similar perks. Some rent furnished homes and include the furniture in the rent. I can see rent for furniture being an extra fee. Perhaps extra fees for things like a refrigerator, a stove, or a dishwasher. Florida law requires rental properties to have functional heating, but not air conditioning. There can be extra fees charged for use of the air conditioner.

This is a situation that was created entirely by government. Businesses respond in a rational way to price controls and increasing costs. Government officials and idiot liberals don’t seem to understand that.