There has been a plethora of stories talking about the privilege possessed by the upper middle class as of late. This article is typical of what the left is trying to do– they are saying that young people no longer have a chance at the American dream because they are being kept down by [insert here: “Boomers,” the upper middle class, banks, landlords, Donald Trump] because of privilege.

The things that supposedly prove that you are blind to your privilege are:

- Why don’t you move to a less expensive area, or one where jobs are more plentiful?

- I worked hard to make it, you can too.

- Money isn’t everything.

- We all have the same opportunities to succeed.

- I don’t worry about money.

- Why don’t they save more?

- Everyone should travel.

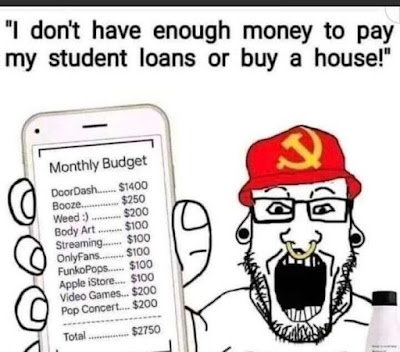

Numbers 1, 2, 4, 5, and 6 are all linked in my mind. It isn’t just about hard work, it’s about choices. The choices that we make directly affect the outcomes that we experience. If you pick a troublesome albatross for a mate, you decide to smoke week all day instead of hustling to improve, or you waste all of your money on OnlyFans, Starbucks, and Door Dash, you are not making good choices. Your outcome will reflect that.

That isn’t to slam having some vices- I like to gamble, and ordering Door Dash when I am at work instead of clocking out for an hour to go eat is actually more cost effective. The think is, you can’t be doing those things when you are poor. The importance of understanding when you can give up wants in order to afford your needs is something that many young people struggle with. Everyone, when they first move out of their parents’ house, is used to living a better lifestyle than they themselves can afford. My mother used to call it a “caviar and Champaign taste on a beer and bread budget.” Live within your means, save as much as you can, and then you will later enjoy a better life. Learn that sacrifices when you are young will pay off when you are older.

Once you realize that, you won’t have to worry about money and you will be able to travel. There is no secret to making it- so many people think that there is some magic or secret society to becoming wealthy, but it isn’t a secret and it isn’t magic.

The way to wealth is this:

Own your house. Renting just means that you are paying someone else’s mortgage.

Buy a house, preferably with a 15 year mortgage. Pay it off as quickly as you can- don’t just make the minimum payments. Look at four different choices (using West Orlando prices):

- Rent a nice 2 bedroom apartment. Ten years ago, it was $1200 per month. Same apartments today are $2300 per month. If you did that for 15 or 30 years, it would cost you $324,000 or $648,000 and you own nothing.

- Buy a house with the roughly same square footage in the same area for $140,000 in 2002. A 5% down mortgage would mean a $7,000 down payment and monthly payments of $937 for 30 years. Total cost for 30 years: $344,320. A lot, but you also now own a house that is now worth $425,000. Not bad. You are now $733,000 more wealthy than if you had rented.

- Or buy the same house with a 15 year mortgage. Now the payments are $1281 per month, but you pay it off in half the time. Now the total cost is: $237,580. After 15 years, no payment at all. You are now $835,000 more wealthy than if you had rented.

- Same 15 year mortgage, but make an extra $200 per month payment against your principal: you pay the house off 3.5 years early, and this saves you another $12,000 in interest payments. You are damned near to being a million bucks ahead of renting.

Don’t pick a spouse/significant other that spends you into the poorhouse.

I know that she (he) is fun- after all, spending money is fun and gives you instant gratification, but at the expense of your future well-being.

Know the difference between wants and needs.

Door Dash, Starbucks, and eating out are great, but you don’t NEED to do that, especially when you are poor. Wait until you can afford it before you waste money on these things. If you don’t own a house, are making extra payments on it, and can’t afford to pay all of your bills plus put at least 10% of your income aside as savings, then you can’t afford to any of those “Wants.” Learn to wait until you can.

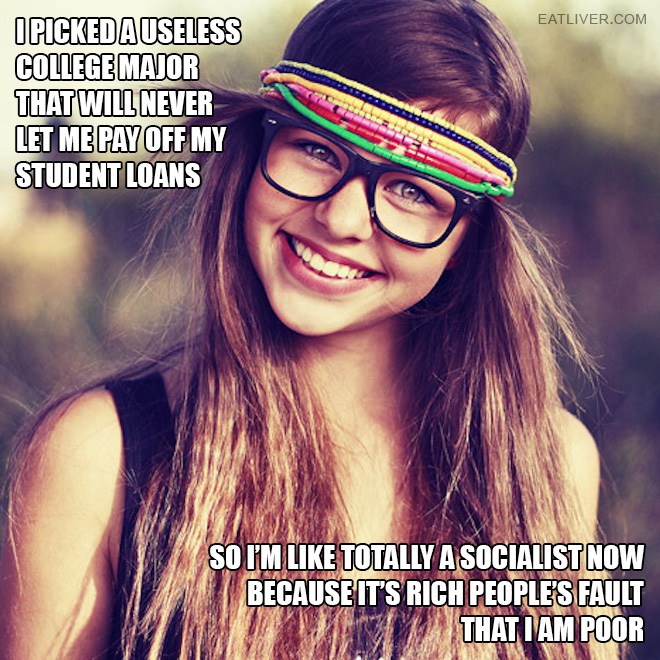

Education is the key to financial well being.

That doesn’t necessarily mean college. The lack of a college degree doesn’t mean that you won’t get a good job. There are plenty of trades out there that make good money- welders, for example. I was a fire medic and making a pretty good living.

Having a college degree doesn’t guarantee you a good job. Taking out $200,000 in student loans for a degree in 14th Century French poetry is a bad idea.

The trick is to learn a valuable skill, then be good at it. Work hard, make wise choices. Save. Don’t waste money on stupid bullshit. Then be patient. It will take a while. It took me about 12 years to go from bankrupt to a million in net worth.

That’s my advice. I have learned all of these things the hard way. It wasn’t privilege that got me to be successful- remember, I have been poor and even homeless. It was the school of hard knocks. Doing the things I recommend here is hard. It takes discipline and sacrifice.

Or you can just stay poor and blame your landlord or Donald Trump for it.

16 Comments

Michael · August 25, 2025 at 6:55 am

As someone that has a paid for house I must demur just a bit in your otherwise excellent wants vs needs story above.

Taxes and repairs. A house isn’t really an investment it’s where you live. MY Cost of Living is LOWER despite the taxes and home repairs (so far) BECAUSE I own not rent. BUT Taxes are RENT on a paid for home.

When NOT IF the local government decides it NEEDS MORE MONEY the Homeowner is the prime target. When infrastructure that the local Government kicked the can on for decades requires replacement the Homeowner is the prime milk cow.

An investment can be sold and proceeds used for other things. Selling my house puts me into the currently insane housing market.

George Carlin had a rant about the “table is rigged” and it’s a big club but you’re not in it. Too long to post here.

Homeowners need to stay connected to the local politics. Eventually you’ll NOT be in the work hard in a good job scenario aka “retirement”. I have a mother in Law apartment here and keep it ready for use PRN for paying utilities and taxes. Otherwise like so many seniors who thought they had a good retirement income plan you get taxed into homelessness.

Divemedic · August 25, 2025 at 7:58 pm

Do you think renters dont pay property taxes?

Woody · August 25, 2025 at 8:16 am

The people who coined the phrase “YOLO”, and spent money they didn’t have are now complaining they don’t have money.

Barry · August 25, 2025 at 8:24 am

Sage advice. Wife and I financed a piece of land and then built and finished out a small garage using my separation pay from the Army. We lived in that garage for 2 1/2 years saving what we could. Finally had the money for the down payment on the house; took out a larger 30-year mortgage plus a small 15-year mortgage to cover the remainder on the land mortgage. Took a second job (drilling in the Army Reserves). Paid off the 15-year mortgage in 3 years and the 30-year mortgage in 10 years.

Lots of pasta and beans and rarely eating out at a restaurant. Worked on my own vehicles (always used), never bought new or name brand stuff, learned the joys of church ministry thrift stores (amazingly good stuff in them and cheap).

Low point was late 2004; just paid our property taxes and, aside from the sacrosanct emergency fund, we had $300 remaining until I received another paycheck. I had just been mobilized back to Active Duty and, unfortunately, our group of mobilized Reservists did not receive a pay check for 60 days as Finance screwed up the paperwork for every single one of us. From that low point, everything improved. It took a decade of building, slowly at first but faster at the end, but life greatly improved.

Now we are doing well and I seek to pay my good fortune forward to others.

Elrod · August 25, 2025 at 8:29 am

Random thoughts: Money – it seems the Educational Industrial Complex is apparently forbidden to teach basic economics. If nothing else, one free period a day with reading assignments – Friedman’s Right to Choose, Sowell’s Basic Economics and Hazlitt’s Economics in One Lesson – would go a long way toward correcting that. So would actual math courses with real math in them.

Mortgage – Few people seem to know how to read an amortization statement on a loan, or for that matter, know that such a thing exists. Even in a 30-year the principal is peanuts for the few several dozen payments, so if nothing else, quintuple pay it when it’s low, then quadruple, then triple, etc. That won’t change a 30 into a 15, but it will fairly easily make it a 20-22 year.

Pay yourself. One of all outgoing payments should be to you, money that’s set aside for “whatever is most important.” Regular savings doesn’t pay much interest, but it is easily obtained. Once a reasonable minimum is reached, start putting it into higher yield – but safe – stuff. Eventually you’ll have something such as a bunch of CDs, each of which matures in sequence; even 4 maturing annually on a quarterly basis before automatically renewing means the longest you have to wait is 90 days; worst case, the CD as collateral will give a lower interest rate on short term loans, very worst case they can be redeemed for face value before maturity sacrifing only the interest.

Real estate is – almost – always a good investment if you know what you’re doing. Many moon ago I worked for an outift that moved us around a lot. If one has a good financial foundation each time you land in a new town, you can hunt down good deals on houses (helps to have a real business already established to do all of this). Find a good property management form to handle it when you get transferred again. Lather, rinse, repeat. A co-worker retired at 22 years – 8 years early, thanks to a corporate buy-out to reduce headcount – with 14 townhouses (3 of which were purchased at foreclosure give-away prices in 2009-2011, thanks the fallout from the 2008 Financial Festivities). Positive cash flow from them is 5X his pension, and over time he has the option to recover the original capital plus the value increase. Which, or course would get re-invested in something else.

The list goes on, but: 1) you have to be smart enough to pursue activities that benefit you; 2) you must be sufficiently disciplined to practice it correctly, and; 3) be patient.

Tsgt Joe · August 25, 2025 at 9:06 am

The vast majority of the crap in my life has been the result of my poor decisions. The good from good decisions. Some things have been easier because I have a higher IQ, many things have been harder because I’ve been burdened by depression and other emotional issues. My youngest sister ( whole family has depression) said it best, in a rant responding to another sisters whining. Depression? Depression! The whole fucking world is depressed, get your ass out of bed, put one fucking foot in front of the other, do it again, all day long. Tomorrow you do the same fucking thing, get out of bed go to work! Though I ended up in a “ touchy feely” profession, social work, my bedrock value has been: a man works, a man provides. To echo little sister, f’ excuses, f’ your sensitive feelings, get to work. With that said, I do have some sympathy for young people who have been sold that bs about needing a college education. But its tempered by the fact that I know a number of folks who got tuition assistance from their employer and paid as they went. I have worked, in addition to other places, the Air Force, General Motors and the state of Michigan. Each one of those offered tuition assistance. Its all about what you do with what you have.

JimmyPx · August 25, 2025 at 9:31 am

I agree with most of your points and you are totally correct on them BUT there are a few things to consider.

First the conditions for young people today are VERY different than when Boomers or even Gen Xers were young. Pensions used to be plentiful and many Boomers retired with a nice pension or got their pension, started a second career and used that extra money to invest.

Now, there are NO pensions except for some government jobs, everyone else is stuck with the crappy 401k for retirement.

Next, much of your wealth was created by the artificially inflated real estate market.

By buying a home when it was cheaper, fixing it up and then selling it during a bubble you could net 100s of thousands of dollars. Unless the Fed drops interest rates practically to zero then that bubble is popping and the real estate market will return to reality. Even still there are NO starter homes anymore, look at the prices right now of houses…totally out of range for most young people. Did you know the average age of a first time home buyer is 38 !!

Finally INFLATION and the stagnation of wages is KILLING young people (and everyone else too).

A kid getting started today making $50,000/year is struggling today even though that was great money when we were young. The thing is that with inflation, that $50,000 was like making $15,000 40 years ago.

I usually agree with you DM, but on this case you are blind to the realization that the goal posts have changed for young people and it is NOT the same as it was for us. FYI THIS is what pisses the younger generations so much about the Boomers especially.

Personally I’m Gen X, late 50s, have no debts except my mortgage which we are paying off. Even our vehicles are paid off and NO credit card debt. I’m fine but I see my young nephews in their 20s working their asses off, doing the right things and can’t get ahead.

Lon Monroe · August 25, 2025 at 10:06 am

Great advice. Partner (female) and I worked for 25 years (both good jobs which paid pretty well) and with no real ‘vacation’ and minimal money spent on ‘want items’: when retired, now live debt free (the key to older age stable living). Now own a small cattle ranch with house, barn(s), all the junk you could possibly image and quite a bit of pastureland. As mentioned already, good choices are key with a dose of common sense (seems to be a bygone thing).

WDS · August 25, 2025 at 11:20 am

Asked a young lady out (years ago) and I said to her “I know this great little restaurant, quiet with excellent food.” She replied, “I’d rather go to the jewelry store at the mall.”

Second date? Hell, there wasn’t even a first date and DM is right, it goes both ways.

SoCoRuss · August 25, 2025 at 11:21 am

Agreed, the current class warfare is also leading to a Dehumanizing campaign now. Whites and especially boomers are to blame for everything. That’s just to make it easier when the time comes to take our stuff for equality.

I fully understand how everything for normal people are high cost now, fuck what the .GOV says.

But, I look at how kids spent now and am shocked. Unless you spend the required $30K (current median cost) for a destination wedding, you aren’t a good parent or don’t love them.

I have a friend with a kid that was just shamed in to paying $5K cost to him to be a best man at a destination wedding. He was already financially shaking but allowed guilt to control him.

You said it, if you cant figure out what to and not to spend money on, you are doomed to failure. But kids have been lead to believe everything to fine, everyone gets a winners trophy, everyone is guaranteed the american dream. It s ALL bullshit but they cant see it so they of course turn to the socialist utopia their college professors pushed as the answer to all ills.

Part of the issue is who is qualified to teach economics/finances in our education system when those idiots say its ok to have massive debt if .gov can print money, then you can have too much debt also.

I don’t just blame the system, parents carry a large portion of the helicopter mentality and not just saying NO to their beautiful little babies…

The last depression was mitigated by lots of folks had families in rural areas who farmed so they could survive, when this depression/collapse hits none of these kids will have a clue on surviving and will die badly or fall in with groups that will make Rwanda look like a spring break party.

Anonymous · August 25, 2025 at 12:10 pm

Be me, fritter away your twenties taking care of sick parents. At end of life of one, finally figure out that you are going to have to take care of you because the rest of your siblings are not going to. Go back and finish STEM degree at 31. Get first degreed job in middle of a recession for low pay. WORK HARDER THAN ANYBODY ELSE and get biggest raise allowed by company but still low man on totem pole. What to do? Unass that AO and move 1100 miles during Hurricane Andrew for new job, new city. WORK HARDER THAN ANYBODY ELSE and also out think them. Ownership recognizes talent and throws raises promotions at you. If they hadnot I would have unassed that AO and gone to another firm. By 40 have accrued spousal unit, daughter, house and $1,000,000 net worth. That was 25 years ago. Nobody handed me nothing but a slim opportunity to succeed. It was a decision to bust my ass to make it happen.

By the way, we only purchased new cars that were a year old non-currents for a huge discount. Kept them for and average of ten years or 150,000 miles. Essentially the cost per year/mile was lower than getting used vehicles. You have to do your research on this and be willing to take whats left in color and option set for whats on the lot. As an example, the truck was purchased on Black Friday 2016, Had 190 demo miles and had been on the lot for 140 days, Stickered for $63k got it for $52k and negotiated trade $500 over book trade value. Picked that specific year because last year of 6 speed tranny. Next year 10 speed and a whole host of problems.

Note to all, Pretty Daughter mentioned earlier, is an IP attorney in San Fran. Paid stupid money but still can’t afford a house. She has “requirements” on where she will live and how. Monthly payment (PITI) on a “nice starter” house will be $17,000. Her current rent is $4000, which she can afford. The kids an insane saver and has a nest egg larger than what I paid for my house originally. The thing is that her DECISION that IP is only done in NYC, DC, Dallas, Chicago, LA or San Fran. If she would entertain doing IP somewhere else, she could get a very nice house for just the nest egg but REASONS in her mind.

Moral to all this is: Make the decision to not be a burden to others and work harder, smarter than the rest of your peers. The decision is first and staying true to it is second.

Spin

@HomeInSC · August 25, 2025 at 12:15 pm

Debt is a tool for you to use and a weapon that can be used against you. Use with care. When the bank will loan you $350k but you can find a perfectly suitable home in a nice neighborhood for $225k, be smart. Leave yourself financial headroom – you’ll be able to handle unexpected events and you will be able to get out of debt sooner.

We had friends who carried over $50k in credit card debt. When houses in our area were appreciating on paper like crazy they refinanced, took out a big pile of cash, paid off their cards, bought new cars, bought new, VERY expensive, diamond wedding rings, and enjoyed fancy tropical island vacations. We moved away and lost touch. I wonder what their current situation is? Old habits die hard. 🙄

Grumpy41 · August 25, 2025 at 1:00 pm

Interesting timing. My assistant (clinical assistant – scribe) just told me “you don’t understand” when it came to hrs in the day and getting assigned work completed.

I just looked at her. 23yo, MAYBE putting in 35 hrs a week. “Ummm, you remember my schedule?? (I routinely work 100-120 hrs a week, there’s 168 hours in a week).” She just blinked. Yeah, don’t tell me about schedules – I work 2FT, 1PT, and 2 PRN jobs.

As Dave Ramsey says – live today like no one else…… so you can live tomorrow like no one else…..

Goergiaboy61 · August 25, 2025 at 1:32 pm

Those young folks who chose unmarketable majors in college and then can’t get ahead in life are worthy of our derision to an extent, but consider the racket that college has become: Alongside viable, economically-useful programs of study in the STEM fields, business/accounting, etc. you have parasitic fields of “victim studies” and so forth which are not only useless economically, but arguably a detriment to society.

A young person who chooses poorly makes a convenient target, but the fact of the matter is that all of us were young and naive at some point, and might have fallen prey to such con-artists and scams.

My somewhat long-winded point is this: What sort of a corrupt and evil enterprise would prey upon people in this manner in the first place? Lying to people, deceiving them, used to be considered shameful, and in some cases, unlawful. If fraud laws were enforced properly, many of these racketeers would be charged with fraud or other financial crimes.

The real reason all of this is such an outrage is that once a mistake of this kind is made, it is often so expensive as to be unrecoverable.

BTW, it is germane to note that I did fine in college and got marketable degrees. But I have spent enough time inside the ivy-covered walls to know the bad as well as the good of the system. And right now, the useful crap is piggy-backing on the useful areas of study. The higher-ed folks get away with that with “general education” requirements that force you to take underwater basket-weaving and whatnot.

The societal cost is starting to manifest itself. Young people caught in this bind aren’t dating and marrying, starting families and having kids, or buying homes as they once did. There are many reasons the Great American Middle Class is in trouble, but this racket is surely one of them.

If you are young and reading this, go to trade school!

georgiaboy61 · August 25, 2025 at 1:34 pm

Re: “And right now, the useful crap is piggy-backing on the useful areas of study.”

Typo alert: “useful” ought to read “useless” for the fifth word into the sentence. My apologies for the error.

Honk Honk · August 25, 2025 at 7:38 pm

Property is theft comrade, AI is printing up the High Speed Rail tickets and UBI.

It’s gonna work this time, we have conquered human nature.

Yes we can, forward!