In a follow up to the credit card post, let’s look at the math of credit card rates. Interest rates on credit cards only matter if you carry a balance on them. Nearly half of credit card holders (47%) carry a month to month balance. Who carries this balance?

- more than half of Gen Xers (ages 46-61; 53%)

- millennials (ages 30-45; 53%),

- 2 in 5 boomers (ages 62-80; 43%)

- Gen Zers (ages 18-29; 40%)

The average balance for credit cards where the owner does carry a balance is $6700.

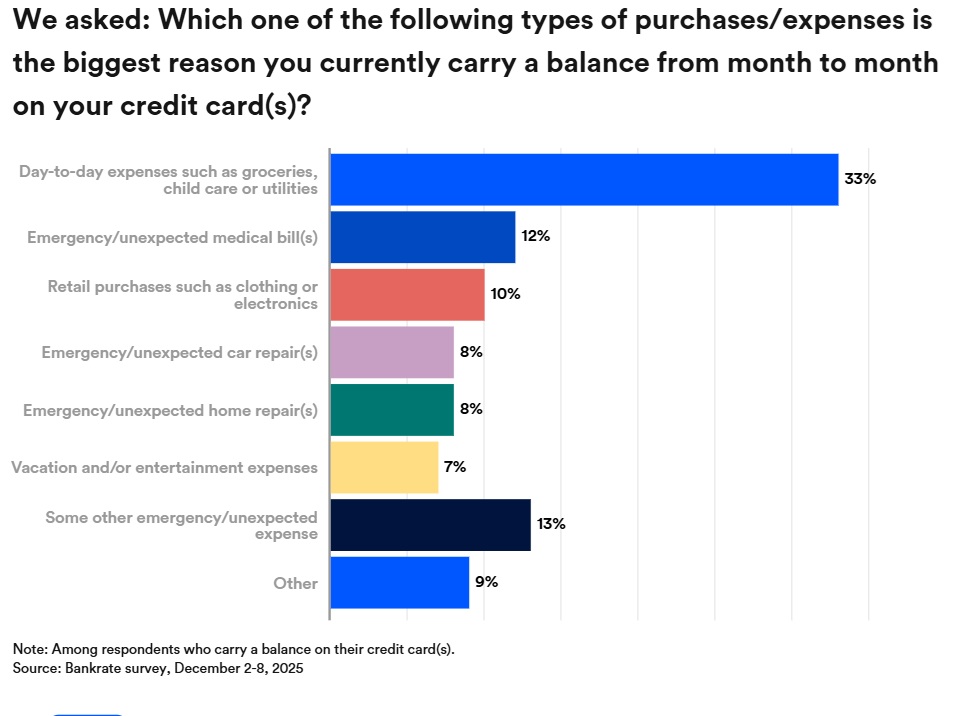

Why do the users carry a balance? The largest single reason is they aren’t properly managing cash flow and spending beyond their means, which forces them to use credit cards for everyday expenses.

According to the Federal Reserve, 82% of American adults have at least one credit card. However, it’s common to have several cards in your wallet. On average, people have 3.9 cards.

My wife and I are super prime users, and we spend about $40,000 per year on credit cards. We use them for everything: utility bills, groceries, you name it. Once, I even made a $20,000 down payment on a car with a credit card. The difference is that we pay the balance off every month. Why do I do that? Rewards.

My Amazon card pays 5% cash back. Our joint card that we use for daily expenses? 5% cash back on fuel and restaurants, and another card gives us 7% credit for use on vacations. It’s all about maximizing our cash back returns. It’s like giving yourself a raise. As for us, that $40,000 a year in card use gets us about $1500 a year in rewards and freebies.

You just have to make sure you don’t carry a balance. That means spending within your means and not carrying a balance. The nationwide average APR on general-use credit cards is 21.91%, which means interest adds up quickly.

Among those who carry a balance, more than 7% of them are more than 90 days past due. So do the math from the other post- people with lower credit scores (below 700) spend the least, but are the most likely to carry a balance and most likely to become seriously delinquent and default.

So Trump’s rule of requiring credit card rates to be capped at 10% will cause credit card limits and availability to be greatly restricted. People will move back to cash, and will have to use debit cards for online transactions. This will in turn do three things:

- It will force people like me to stop taking advantage of rewards, because they will no longer be available. I, and other prime and super prime users, will have to switch back to cash.

- Prime users with scores between 700 and 749 will have restricted access to cards, and even then, those cards will have very low spending limits, likely $1000 or less.

- Credit cards will simply not be available to those with a credit score below 700. This will force these subprime borrowers into more expensive payday loans, which carry interest rates of more than 300%.

The hit to online vendors and shopping will be enormous. Amazon, as the world’s largest online retailer with $400 billion in annual online sales, will be especially hard hit as people lose access to easy digital funding sources.

Likely, this will eventually settle into digital currency becoming more popular. At that point, I will have to reevaluate my opinion of things like bitcoin.

Just remember- price controls NEVER work as intended. Where there is market demand, the market will find a way to supply that demand.